{kind=link}

User-first overview

For many drivers and small merchants, a quick credit line is less about bells and whistles and more about cash flow and predictability. This guide frames DiDi’s lending product from the user’s point of view — eligibility, onboarding steps, and what to expect from the user experience. For hands-on details and to compare features, check didi finanzas early in your evaluation.

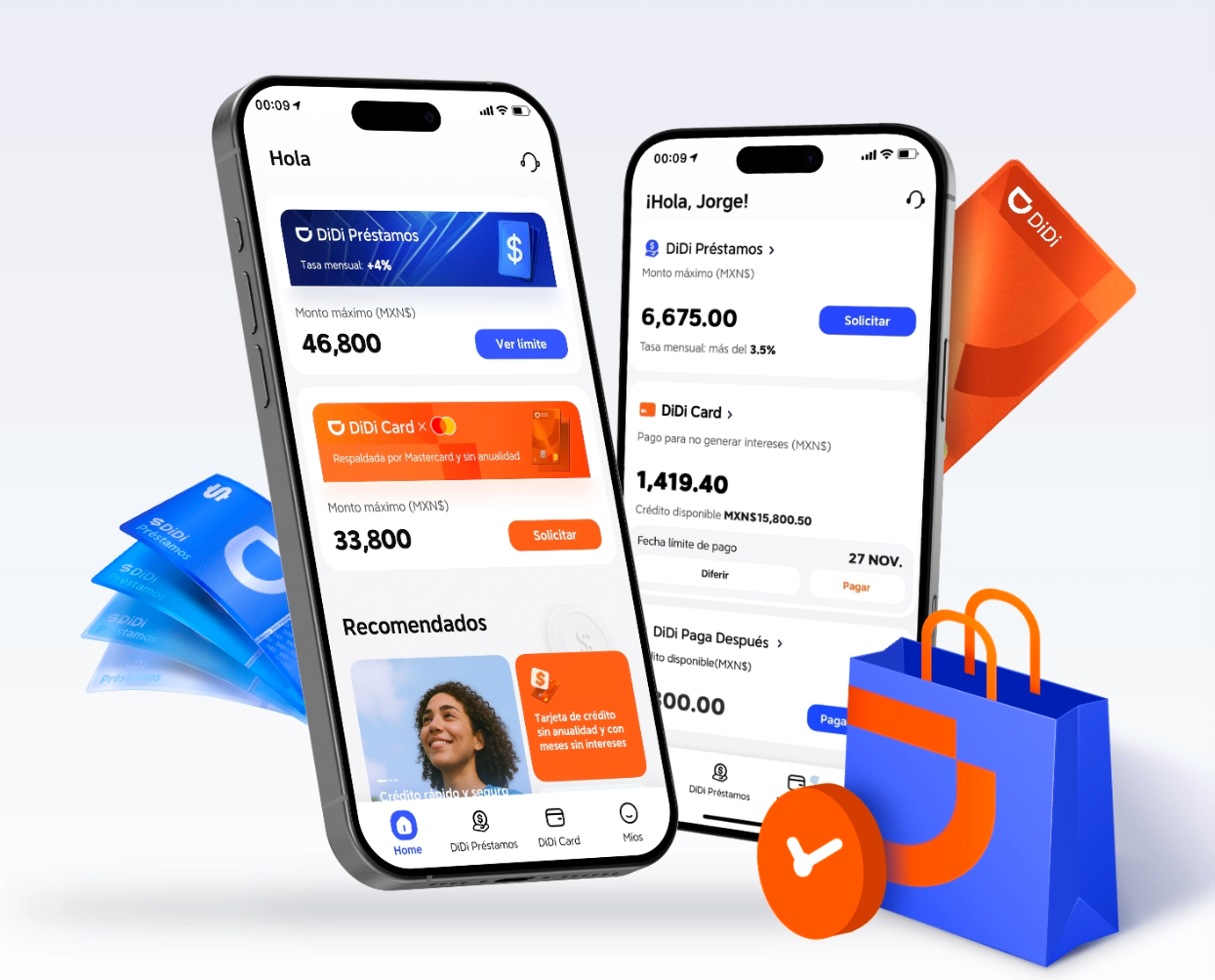

How DiDi’s digital credit product functions

DiDi packages short-term credit inside its platform so approvals happen within the app. Underwriting leverages ride-history, transaction telemetry, and soft credit signals rather than heavy paperwork. The flow typically includes KYC verification, automated credit scoring, and an instant disbursement option. If you want to preview the interface and specific product terms, explore the didi finanzas app for screenshots and sample APR ranges.

Core eligibility and documentation

Expect a streamlined checklist: valid ID, proof of bank account for disbursement, recent activity on the DiDi platform (rides or deliveries), and sometimes a minimum tenure as a driver or partner. The algorithm substitutes many manual checks with platform-derived signals; still, basic KYC and consent for a soft bureau query are standard. Industry terms like underwriting, credit bureau, and APR will surface in your summary page — know them, but focus on the concrete items listed.

Onboarding checklist: steps that move the needle

Follow these concrete actions to reduce friction during approval: authenticate your identity, sync your bank account, maintain steady platform activity for 30–90 days, and respond promptly to any verification prompts. Keep ride logs and recent bank deposits accessible in case manual review is triggered. Onboarding is API-driven on the backend, so delays usually trace back to missing documents or mismatched account names.

Common pitfalls and sensible alternatives

Borrowers often underestimate price vs. convenience — a fast fund is useful but can carry higher APRs or fees. Another common mistake is applying for multiple micro-loans simultaneously; that fragments repayment capacity and can harm future access. — Remember to compare total cost over the term, not just the headline fee. If DiDi’s terms feel steep, consider short-term bank credit, credit unions, or other app-based lenders with transparent repayment schedules as alternatives.

Security, pricing transparency, and user control

DiDi’s lending model should provide an itemized payment schedule and clear consent screens. Look for explicit disclosure of interest rate, repayment frequency, late fees, and prepayment rules. From a security standpoint expect encrypted data transfer and standard authentication on payouts. If anything in the interface feels ambiguous, pause and request a breakdown — that single step prevents surprises in billing.

Real-world anchor and market context

Across Mexico City and other major urban centers, app-based microcredit has become a practical bridge for gig workers managing variable income — a pattern intensified after the 2020–2021 fintech growth surge in Latin America. That local context explains why platforms built lending flows directly into driver dashboards: operational data correlates closely with repayment capacity, which simplifies credit decisions on the supply side.

Common metrics to vet before you accept credit

Evaluate these three critical metrics before committing: effective APR (total annualized cost), repayment cadence alignment with your cash inflows, and any origination or servicing fees that inflate the headline rate. Also confirm how missed payments affect access to future credit and whether the lender reports to credit bureaus — those mechanics shape long-term credit health.

Advisory: three golden rules for selecting the right digital credit

1) Prioritize total cost over speed: calculate total repayment and compare across offers. 2) Match the repayment frequency to your cash cycle: weekly gig income often favors weekly installments. 3) Validate transparency: require an itemized amortization schedule before you accept funds.

DiDi Finanzas sits naturally as the integrated solution when you need short, predictable lines that tie to platform earnings — the product is most effective when used on purpose and with the numbers clear. — Practical choices beat flashy promises every time.